26 Aug 2025

Have you ever reviewed your paycheck and wondered why the disposable amount appears smaller than expected? You are certainly not alone. For many expats working in the UK, understanding how much money you truly get. After-tax and contribution matters more than you might expect.

The main idea of this post is to help you understand your pay. It covers gross pay, deductions, and ways to increase your take-home pay. This knowledge can help you plan better. This knowledge can help you save smarter and send money home with ACE Money Transfer.

Let’s break it down:

Component | Amount |

Gross (salary) | £28,000 |

Tax & NI & Pension | – ~£5,000 |

Net pay | £23,000 |

According to HMRC (2025), the personal tax-free allowance is £12,570—it means the first chunk of your earnings isn’t taxed. It affects how much goes from gross to net directly. Knowing this clears up why expected earnings feel lighter in reality.

Learning this difference is critical for expat workers. Your net pay is your actual resource for rent, savings, and most importantly, sending support back to family.

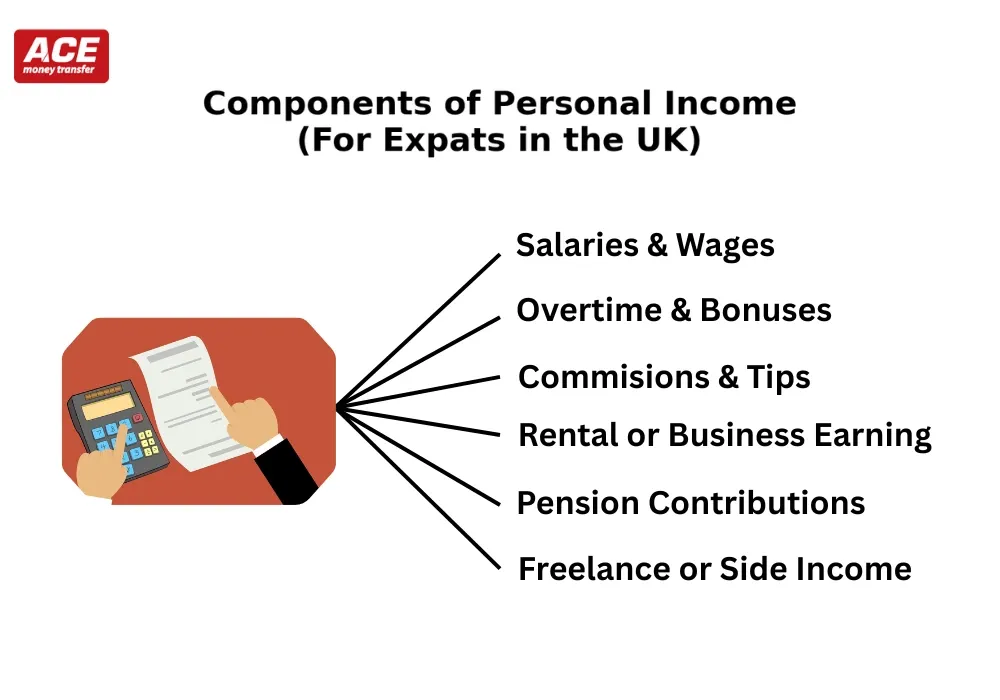

When thinking of earnings, don’t stop at base salary. A full income picture includes:

Why detail every source? It helps you see how much you significantly bring in each month. For example:

The Office for National Statistics (2024) placed the UK full-time pay average at about £34,000 annually. Useful for comparing with your overall earnings. Once you map out what “counts,” you can set clearer budgets, track savings, and plan remittances more truthfully.

You might not immediately increase your gross pay, but you can influence how much actually lands in your account by:

Let’s say you contribute £100/month to a pension. This lowers what HMRC taxes now, giving more net pay or potentially bigger refunds later. If you’re unsure, HMRC’s website or your payroll team can guide your steps.

Fine-tuning deductions and contributions isn’t just numbers. It affects your daily life and your family back home:

For example, adding a little more to your monthly pension can lower your taxes now while still giving you enough take-home pay. In turn, that steady planning helps you send consistent support to loved ones using a trusted service like Send money online.

If your net pay is, say, £1,600 or £2,200 per month, you need full clarity to manage:

With a clear view of pay versus real resources, you can choose the right platform and timing to remit money, optimizing exchange rates and fees. For example, a blog like “How to Calculate Your Yearly Earnings” offers more insights on planning finances. Combine that knowledge with knowing your net income, and you’re well on your way to sound financial decisions.

Here are simple, effective practices tailored for you:

Starting from the difference between your gross pay and your real take-home, tracking every source of income, and fine-tuning your tax or pension setup empowers you. It helps not only to smooth your life in the UK. But to make every remittance count.

Understanding your true pay means you can confidently send money online in seconds. Fast, secure, and designed for hardworking expats like you.

It’s adjusted for tax, NI, pension contributions, and any lawful deductions.

Yes. Legally claim for travel, tools, or home office costs to lower taxable income.

They lower your taxable income now, which means less tax now and more savings later.

Yes. HMRC allows you to claim refunds of overpaid tax.

Knowing net pay vs. gross helps in budgeting, planning remittances, and avoiding last-minute financial strain.

To read more related blogs at gross income vs net income difference.