29 May 2026

Whether you're receiving money from family abroad or sending funds internationally from your Barclays account, one piece of information stands between you and a smooth transfer: the right bank code. The Barclays SWIFT code — also called the Barclays BIC code or Barclays bank Swift codes — tells the global banking network exactly where to route your money. Get it wrong, and your transfer could be delayed, returned, or sent to the wrong place entirely. This guide covers everything you need to know in plain English.

UK banking uses several types of codes, each designed for a specific purpose.

• Sort code: a six-digit number used for domestic payments within the UK

• Account number: used with the sort code for everyday UK transactions

• IBAN (International Bank Account Number): identifies your account for international transfers

• SWIFT/BIC code: identifies Barclays in the global banking network for cross-border payments

Each code has its place, and understanding which one applies to your situation saves time and prevents costly errors. SWIFT stands for the Society for Worldwide Interbank Financial Telecommunication, a secure messaging system banks use to send encrypted payment instructions rather than moving physical cash, and SWIFT and bic codes are the same identifier in this context. To put this in context, the SWIFT network currently connects over 11,000 financial institutions across more than 200 countries and territories, processing millions of payment messages every single day. These codes standardize international transactions and support faster, more secure processing and record-keeping.

The terms SWIFT code and BIC code mean the same thing and are used interchangeably across the industry. SWIFT stands for the Society for Worldwide Interbank Financial Telecommunication — the global network that processes payment instructions between banks. BIC stands for Bank Identifier Code, which is the official ISO 9362 term for the same identifier. Together, they form the backbone of international wire transfers.

Barclays operates two main legal entities in the UK, each carrying a different primary SWIFT/BIC code:

| Entity | SWIFT/BIC Code | Purpose |

|---|---|---|

| Barclays Bank UK PLC | BUKBGB22XXX | Personal and business retail accounts |

| Barclays Bank PLC | BARCGB22XXX | Corporate and investment banking |

For most personal account holders, the main code for Barclays Bank is BUKBGB22, which is the code most personal customers use. This is confirmed on Barclays’ own website for receiving payments from overseas. Individual Barclays Bank branches, including some local branches, may also carry branch-specific codes (such as BARCGB22TPS for a particular location), but using the 8-character head office version for international transfers usually avoids complications tied to unique branch codes. Confirm the correct code with Barclays or the recipient before sending.

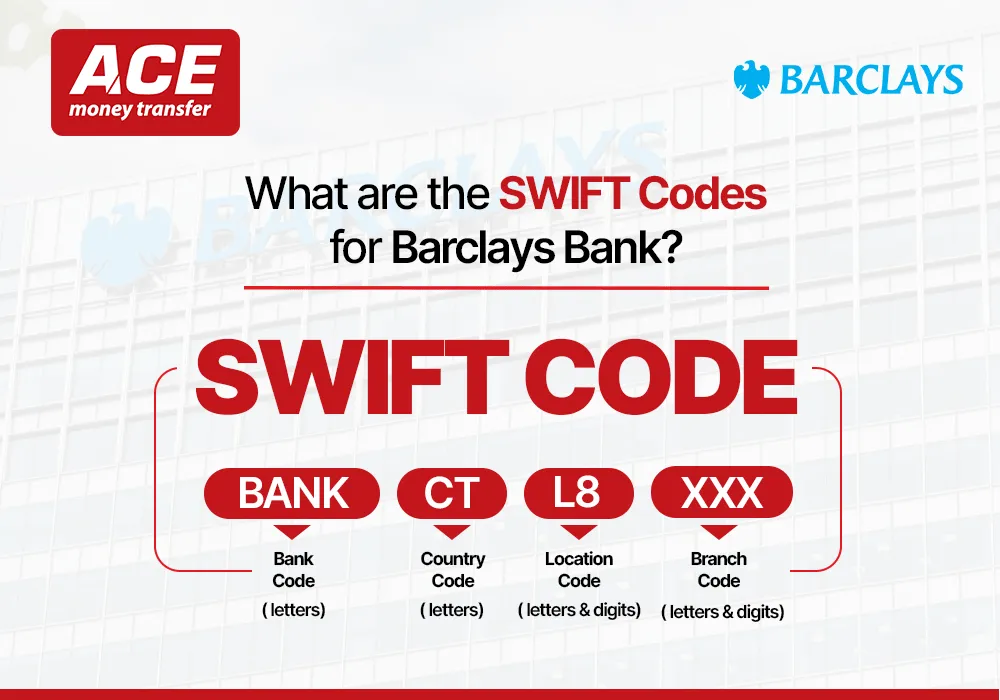

All SWIFT codes follow a strict 8 or 11-character format. Here is how BUKBGB22XXX breaks down:

• Bank Code (4 letters): Identifies the bank, e.g. BUKB or BARC for Barclays

• Country Code (2 letters): Shows the country, e.g. GB for United Kingdom

• Location Code (2 characters): Indicates city or head office, e.g. 22 for London

• Branch Code (3 characters, optional): Identifies branch, XXX means head office

Example: BUKBGB22XXX = Barclays (UK, London, Head Office)

An 11-character code with a specific branch suffix directs a transfer to a named branch. An 8-character code, or one ending in XXX, routes the transfer to Barclays' primary office, which then processes the payment to the correct account. If you're ever uncertain, the 8-character head office code is the safe default.

| SWIFT/BIC Code | Entity | Use Case |

|---|---|---|

| BUKBGB22XXX | Barclays Bank UK PLC | Personal/retail transfers (most common) |

| BARCGB22XXX | Barclays Bank PLC | Corporate and investment banking |

| BARCGB22TPS | Barclays Bank PLC (branch) | Specific branch-level transfers |

The sort code is the foundational routing number for all UK domestic payments. Every Barclays branch has a unique six-digit sort code — the first two digits identify Barclays as the bank, and the remaining four pinpoint the branch and location. You'll find your sort code on the front of your debit card, within your online banking dashboard, on your bank statements, and at the bottom of any cheque.

For international transfers, the sort code is not used independently. Instead, it is embedded within your IBAN — occupying characters 9 to 14 of the 22-character UK IBAN string. When you give a sender your IBAN, they automatically have your sort code as part of it. You do not need to provide the sort code separately for overseas payments.

The UK IBAN is always 22 characters long. For a Barclays account, it follows this structure:

Example: GB29 BARC 2006 0549 6819 58

• GB — Country code for Great Britain

• 29 — Two-digit check number (calculated algorithmically to catch errors)

• BARC — Bank identifier, drawn from the first four characters of the Barclays BIC

• 200605 — Your six-digit sort code

• 49681958 — Your eight-digit account number

The check digits at positions three and four are particularly important. They're calculated using a mathematical algorithm that catches most transcription errors before a payment is processed. This is one reason the IBAN system is more reliable for international transfers than using a raw account number.

You can generate your personal Barclays IBAN through Barclays Online Banking, the Barclays mobile app, or via the IBAN generation tool on Barclays' website. It is also printed on your bank statements. The IBAN remains the same for any given account — it does not change unless you change accounts.

| Code Type | Example | Length |

|---|---|---|

| Barclays IBAN | GB29 BARC 2006 0549 6819 58 | 22 characters |

| Barclays SWIFT (retail) | BUKBGB22XXX | 8–11 characters |

| Barclays SWIFT (corporate) | BARCGB22XXX | 8–11 characters |

| UK Sort Code | 20-00-00 | 6 digit |

For payments within the UK, only a sort code and account number are needed. The UK's Faster Payments system processes most domestic transfers in seconds, and it operates 24 hours a day, seven days a week. Setting up a direct debit, sending money to a friend, or receiving your salary all rely solely on these two pieces of information. No IBAN or SWIFT code is involved in domestic UK transactions.

Sending or receiving international money with a Barclays account requires key details for a successful international transaction, such as your IBAN, the Barclays SWIFT/BIC code (BUKBGB22), and your full account name. For USD transfers, you may also need Barclays’ correspondent details, including the ABA/Fed Wire number 026002574.

Outgoing international payments from Barclays usually require the recipient’s IBAN (where applicable), SWIFT/BIC code, bank address, and name; if any SWIFT/BIC or account details are unclear, double-check with the recipient or the recipient's bank before sending. Transfers typically take 2–5 business days to process, and SWIFT/BIC codes are globally unified identifiers that help prevent delays, rejections, or extra fees when the correct bank details are used.

However, costs can be high—according to the World Bank Remittance Prices Worldwide (Q1 2025), banks charge an average of 9.50% for a $200 transfer, compared to about 3.65% for digital money transfer services, highlighting the importance of choosing the right method for international payments. If you need to verify any detail, contact Barclays or the recipient to confirm the correct bank information before sending.

Still have questions? Explore Barclays Transfer Time & Fees for more info.

Knowing precisely which code to use — and when — prevents delays and back-and-forth with your bank.

• Use your sort code and account number for all domestic UK payments: paying a bill, setting up a standing order, or receiving a salary payment from a UK employer. These are the only codes the UK's payment rails need.

• Use your IBAN when receiving a payment from a country that recognises the IBAN system — primarily European nations — or when making a SEPA credit transfer to a eurozone bank account. For SEPA transfers, the IBAN is mandatory.

• Use the Barclays SWIFT code (Barclays routing code SWIFT) for any international wire transfer. Whether someone is sending money to your Barclays account from India, Pakistan, Canada, or Australia, the SWIFT code is what tells their bank where to send the funds. If you're sending money abroad from Barclays, you'll need the recipient bank's SWIFT code on their end.

• Use the USD correspondent details (ABA 026002574) only when receiving a USD wire from outside the UK, as the funds pass through a US correspondent bank before reaching your Barclays account.

Both the UK and Europe use IBAN, making cross-border transfers between them more straightforward than with non-IBAN countries. However, the structures differ. UK IBANs are 22 characters; German IBANs are 22, French are 27, and Italian are 27 characters. The UK IBAN uniquely embeds the sort code — a feature tied to the British banking system. European IBANs embed their own national bank and branch identifiers. Despite the structural variations, both formats are read by the same global IBAN processing system.

The United States uses a nine-digit ABA routing number to identify banks and branches — functionally similar to a sort code, but formatted differently. The US does not use IBAN at all. When sending money from the US to a Barclays account, the US sender provides their ABA routing number on their end, while the Barclays account holder provides their IBAN and the Barclays SWIFT code. For USD transfers, Barclays' ABA intermediary number (026002574) may also be required.

India uses the Indian Financial System Code (IFSC) — an 11-character alphanumeric code — for domestic bank transfers through NEFT and RTGS. India does not use IBAN. When sending money from the UK to India, the recipient provides their IFSC code and account number rather than an IBAN. India is the largest single destination for remittances from the UK, making this corridor particularly relevant for many UK residents.

The Migration Observatory at Oxford University confirmed that India and Pakistan were the top two destinations for UK remittances in 2024 — and also the cheapest corridors, with bank transfer costs falling below 1% in some cases. In fact, global remittances to low- and middle-income countries reached $685 billion in 2024, growing by 5.8% year on year — with South Asia recording the highest regional growth at 11.8%.

There are several easy ways to confirm the right code, including using Barclays sources to search for the correct details:

• Barclays App or Online Banking: Log in and go to your account details or international payments section. The SWIFT/BIC code is listed alongside your sort code and account number.

• Your Bank Statement: SWIFT codes often appear on statements, especially if you have previously received an international payment.

• Barclays’ Official Website: The most reliable source is always Barclays directly. Visit barclays.co.uk to search for the right SWIFT/BIC details by account type or branch information, or the latest confirmed code.

• Call Barclays Customer Service: If you are unsure, contact Barclays support and ask them to confirm the right code for your specific account type or payment purpose.

Tip: Always double-check the SWIFT code before confirming your transfer. Even a small mistake can delay your payment or send it to the wrong branch, so it’s worth taking a few extra seconds to verify it carefully.

Small errors like using the wrong SWIFT code, sort code, or missing IBAN can delay or reduce your international transfer.

One of the most common mistakes is entering the wrong SWIFT code. Barclays has two main entities:

• Barclays Bank UK PLC (BUKBGB22XXX)

• Barclays Bank PLC (BARCGB22XXX)

If you use the wrong one, your transfer may be delayed or sent back. Most personal accounts use BUKBGB22. If you are unsure, always confirm with Barclays before sending a large payment.

Another frequent mistake is putting the sort code in the SWIFT/BIC field.

• The sort code is only for UK domestic payments

• SWIFT code is required for international transfers

These two are not interchangeable.

Some people only provide their account number for international transfers. This is incorrect.

• Overseas banks need the full IBAN

• UK IBAN has 22 characters

• Account number alone cannot be used for international payments

Many people forget about extra charges during international transfers, including visible bank costs and hidden fees.

• Money may pass through one or more intermediary banks

• Each bank can deduct a fee

• The final amount received may be lower than expected

According to the Financial Conduct Authority (FCA), hidden exchange rates and intermediary charges can cause UK customers to lose 3% to 5% of their transfer value. Neither Barclays nor any transfer provider can guarantee the full amount received when intermediary deductions or FX spreads apply.

Yes — sharing your IBAN, SWIFT/BIC code, and sort code is entirely safe. These are routing identifiers, not security credentials. They tell the banking network where to direct funds; they cannot be used to withdraw money or access your account. Banks, employers, and payment platforms ask for this information as a matter of routine.

Your sort code and account number are already printed on every cheque you issue and on the front of your debit card, so they have never been considered sensitive data. The same logic applies to your IBAN and SWIFT/BIC — they are public-facing identifiers used to receive money, not private keys that protect your account.

What you must never share are your online banking password, your card PIN, one-time passcodes, or full card numbers. Those are the credentials that actually secure access to your funds.

Understanding the Barclays SWIFT code is only half the picture. The other half is knowing how much your international transfer actually costs — and whether there’s a better way. Notably, the UK digital remittance market alone was valued at $1.53 billion in 2024 and is projected to grow at a compound annual growth rate of 16.7% through to 2030, reflecting a clear shift away from expensive bank transfers toward faster, cheaper digital alternatives.

ACE Money Transfer is built for exactly this purpose. Trusted by the UK diaspora community for fast, transparent, and affordable money transfers to countries including Pakistan, India, Bangladesh, the Philippines, and many more, ACE offers competitive exchange rates and clear fees with no hidden fees. Better rates and transparent pricing can also lead to savings compared with traditional bank transfers. You don’t need to look up a SWIFT code or worry about correspondent bank deductions — ACE handles the routing, compliance, and currency conversion on your behalf.

Visit ACE Money Transfer today to compare rates, check delivery times, and send money home with confidence.

The Barclays SWIFT code is an 8 or 11-character identifier used for international transfers. For personal accounts under Barclays Bank UK PLC, it is BUKBGB22XXX. For corporate accounts under Barclays Bank PLC, it is BARCGB22XXX. It is also called the Barclays BIC code or Barclays bank identifier code.

Yes. All UK Barclays accounts have a 22-character IBAN. It begins with GB, followed by two check digits, the bank code BARC, your sort code, and your account number. You need it to receive international payments and for SEPA transfers from European banks.

Yes, for virtually all international wire transfers. The Barclays international transfer code tells the sending bank which UK financial institution to route the payment to. Some digital transfer services handle SWIFT routing automatically, so the sender only needs to enter basic recipient details.

Barclays SWIFT codes are 8 or 11 characters. The 8-character version (e.g., BUKBGB22) refers to the head office and is the most commonly used. The 11-character version includes a three-character branch suffix (e.g., BUKBGB22XXX or a specific branch code).

For domestic UK transfers, yes — a sort code and account number are all you need. For international transfers, the Barclays overseas transfer code (SWIFT/BIC) is required in nearly all cases. Some fintech remittance platforms simplify this by managing the SWIFT routing on the sender's behalf.